Global Base Oil Price prediction: Price Projections for 2026, 2027, and Beyond

Date: February 12, 2026

The global base oil market is currently navigating a period of heightened volatility and structural transformation. As of early 2026, industry stakeholders are balancing a fundamental supply-demand imbalance against significant geopolitical risks that threaten to upstrip standard market modeling. This report provides a comprehensive analysis of the price trajectory for base oils through 2030, localized within the current macroeconomic climate.

1. Geopolitical Risk Assessment: The Middle East Factor

As of today’s date, February 12, 2026, the primary catalyst for price “spikes” remains the escalating insecurity in the Middle East. While the market is fundamentally well-supplied, the threat of maritime disruptions near the Strait of Hormuz has reintroduced a significant “war premium.”

-

Supply Chain Vulnerability: Increased regional tensions threaten the output of the Largest Base Oil Producers.

-

Refining Correlation: Any disruption in crude flows directly impacts the Base Oil Production Process, as refiners prioritize high-demand fuels. This often leads to a sympathetic rise in Gasoline articles and Kerosene articles, further squeezing lubricant margins.

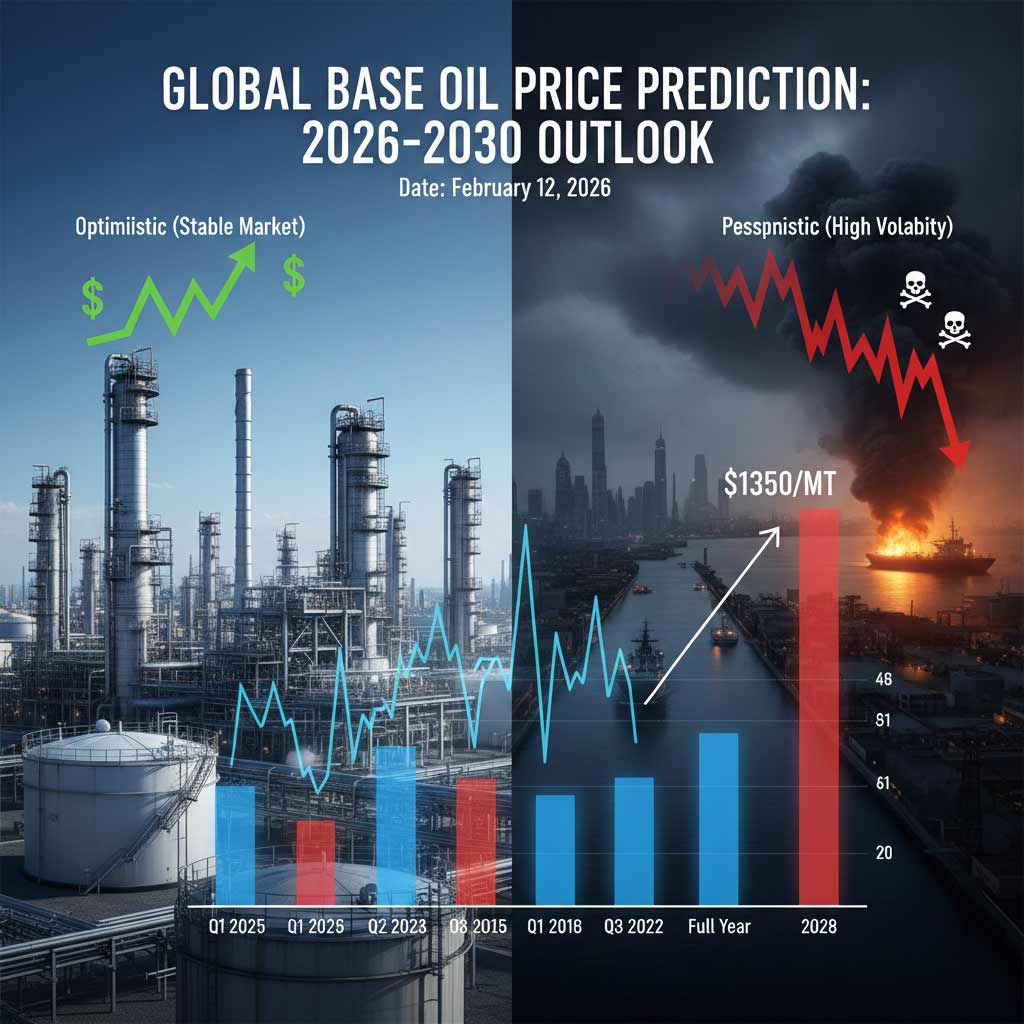

2. Multi-Year Price Drivers and Forecasts

2026-2027: The Surplus Era

The immediate horizon is defined by a “supply glut” as new capacities in Asia and the U.S. come online.

-

Factors: Slowing internal combustion engine (ICE) sales and the rise of high-performance Group III oils are leaving Group I and Group II stocks in a state of oversupply.

-

Optimistic (Bearish for Sellers): If trade tensions ease and production remains disciplined, prices could stabilize at $850–$900/MT.

-

Pessimistic (Bullish for Sellers): Should Middle East insecurity lead to a sustained export halt, prices could surge toward $1,350/MT due to panic-buying and logistics surcharges.

2028: The Structural Shift

By 2028, the market will likely see the impact of refinery rationalization.

-

Factors: As older Group I plants close, the supply of byproduct Sulfur articles and base stocks will tighten.

-

Scenario: If the global economy enters a high-growth phase, a “Supply Crunch” could push average prices to $1,200/MT. Conversely, a global recession could see prices languish at $800/MT.

2030: Long-Term Equilibrium

The 2030 outlook is dominated by the energy transition and carbon pricing.

-

Factors: The maturation of the EV market will significantly dampen the demand for traditional engine oils.

-

Scenario: In an “Accelerated Transition” (high EV adoption), base oil may become a specialty niche product priced at $1,100/MT due to high production costs. In a “Delayed Transition” scenario, prices could reach $1,450/MT as supply falls faster than demand.

3. Comparative Price Forecast Table (2025–2028)

The following data represents the projected average for Group II Base Oil (USD per Metric Ton), factoring in current Base oil articles market sentiment.

| Period | Optimistic (Stable Market) | Pessimistic (High Volatility) |

| Q1 2025 (Reference) | $1,010 | $1,050 |

| Q2 2026 | $890 | $1,150 |

| Q3 2026 | $860 | $1,280 |

| Q4 2026 | $840 | $1,320 |

| Full Year 2027 | $920 | $1,180 |

| Full Year 2028 | $1,050 | $1,350 |

4. Strategic Deep Dives

For professional traders and procurement officers, understanding the interplay between different energy sectors is critical. We recommend reviewing the following technical resources:

-

Market Fundamentals: See our Introduction to base oil for a breakdown of API groups.

-

Supply Side: A detailed list of the largest base oil producing countries and top oil producers.

-

Cross-Commodity Trends: Our latest gasoline price forecast in 2026 and 2027 provides essential context for refining spreads.

-vs.-Coal")

Leave a Reply

Want to join the discussion?Feel free to contribute!